Even though 70% of India’s population inhabits rural areas, commerce has been rigidly focused on urban areas. The status quo approach is being inverted, though, as urban markets become increasingly saturated and companies’ views of rural markets are revised.

Rural Indian markets, whose potential has historically been dismissed, house 700 million people and account for more than 50% of fast-moving consumer good (FMCG) sales, and 60% of the durables market. The annual size of the rural market for FMCGs has been steadily growing and is estimated at $11 billion (pg. 3).

The shift to rural markets has only recently begun in full force as companies have realized that it is too costly to ignore this market any longer. While the per capita income of rural India is half what it is in urban India, disposable income does not follow suit. In fact, surplus disposable income is roughly the same, with the rural consumer paying virtually nothing for health, education, housing and food.

In overcoming the difficulties of penetrating rural markets, companies are turning to the rural poor not only as potential consumers, but as retailers as well. Collaborating with microcredit clients has proven to be good business.

The most revolutionary example of such partnership is between Indian company Hindustan Lever Limited (HLL), a subsidiary of Unilever, and CARE India’s multi-state microfinance program. By linking HLL with self-help groups throughout India, women have received training in retail and marketing to sell staple products in rural, low-income areas.

The joint venture, named Project Shakti, has already expanded to 12 states and aims to include 40,000 (up from 16,000) women by next year. By penetrating rural markets through access points such as microfinance institutions, an important catalyst to increase scale is emerging, with immense potential for future growth.

Additional Resources

1) Main article discussed in entry, Wall Street Journal: "With Loans, Poor South Asian Women Turn Entrepreneurial."

2) "HLL Inks Strategic Alliance with CARE India."

3) Book Review: "The Fortune at the Bottom of the Pyramid," C.K. Prahalad

4) Financial Express: "Competing Visions of Rural India."

Based on data collected from projects in India, Ghana and Pakistan that aim to improve financial inclusion for rural women, the authors examine the interplay between gender dynamics and the employment of women as agents supplying in cash-in and cash-out (CICO) services. This includes the impact these agents can have on communities, the challenges faced by women in becoming and succeeding as agents, and possible solutions to these challenges.

Based on data collected from projects in India, Ghana and Pakistan that aim to improve financial inclusion for rural women, the authors examine the interplay between gender dynamics and the employment of women as agents supplying in cash-in and cash-out (CICO) services. This includes the impact these agents can have on communities, the challenges faced by women in becoming and succeeding as agents, and possible solutions to these challenges. Andrij Fetsun, Founder & CEO at AFI:

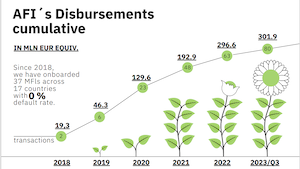

Andrij Fetsun, Founder & CEO at AFI: